.png)

The Rise, Rewards, and Risks: Navigating the Private Credit Boom.

With assets under management in private credit strategies nearing $2 trillion, the sector is no longer the financial markets' best-kept secret. But as interest rates rise, the landscape is shifting. Deals like Oak Hill Advisors, Blue Owl Capital, and HPS Investment Partners are providing a breaking record of $5.3 billion loan package to a fintech firm, Finastra, Ares Management's $3.5 billion loan portfolio from PacWest and KKR's $44 billion consumer loan acquisition from PayPal are just the tip of the iceberg.1 Here's what you need to know…

First, let's understand Private Credit as an Investment Opportunity:

Private credit, a misunderstood asset class, has emerged as a promising alternative for investors seeking diversification and yield in today's complex financial landscape.

What is Private Credit?

Simply put, private credit refers to debt agreements made privately between borrowers and lenders, without trading on public markets. These loans are typically illiquid but can offer higher yields compared to their public counterparts.

Why Consider Private Credit?

Enhanced returns on Debt: Private credit funds tend to promise higher returns than listed fixed income, but with similar mechanics of debt, such as being asset backed, having fixed terms and providing fixed coupons.

- Diverse Opportunities: From senior debt to preferred equity, to distressed debt, private credit offers a range of investment types, each with its unique risk and return profile.

- Growing Market: With banks retrenching from traditional lending roles, private credit funds are stepping in, filling the gap and offering flexible solutions to borrowers.

Who's Who in Private Credit?

Success in private credit hinges on a manager's ability to originate deals, their industry expertise, and their networking capabilities. Top-tier managers differentiate themselves through these attributes. Some of the biggest private credit funds include Ares Management Corporation, Oaktree Capital Management, L.P., The Carlyle Group, Blackstone, Sixth Street, and Bain Capital Credit.

While private credit offers many opportunities, it's not without its challenges. Terms like 'mezzanine' and 'lien' can be daunting for newcomers. However, with the right guidance and understanding, investors can navigate this landscape confidently.

Here's a simplified guide to help you navigate:

- Direct Lending: These are loans provided directly to businesses, often for purposes like growth, acquisitions, or refinancing.

- Real Estate Lending: While technically a form of direct lending, the prominence of this strategy warranted its own bullet point. This involves providing first or second mortgages to developers, high net worths or corporates backed by real-estate.

- Venture Debt: This is specialized financing for venture-backed startups, usually as a supplement to equity financing.

- Distressed & Special Situations: These are investments in companies facing challenges but offer potential for high returns upon recovery.

- Mezzanine Financing: This is a hybrid form of capital that sits between senior debt and equity, often including options for equity conversion.

Exhibit 1: The Meteoric Rise

The growth in private credit assets under management is nothing short of phenomenal. With capital flowing into various sub sectors, the market is maturing at a rapid pace, offering a plethora of opportunities for investors.

The Paradox of Yield Chasing

High yields in private credit are enticing for investors but can be a double-edged sword. These attractive returns come at a cost—higher repayment rates for borrowers. As Exhibit 2 shows, high bond yields have led to rising default rates. While private lenders have tools to mitigate defaults, such as extending loan terms, these can dilute investor returns. So, high yields are not without their risks.

Exhibit 2: Default rates for private credit, leveraged loans and high yield in U.S. markets

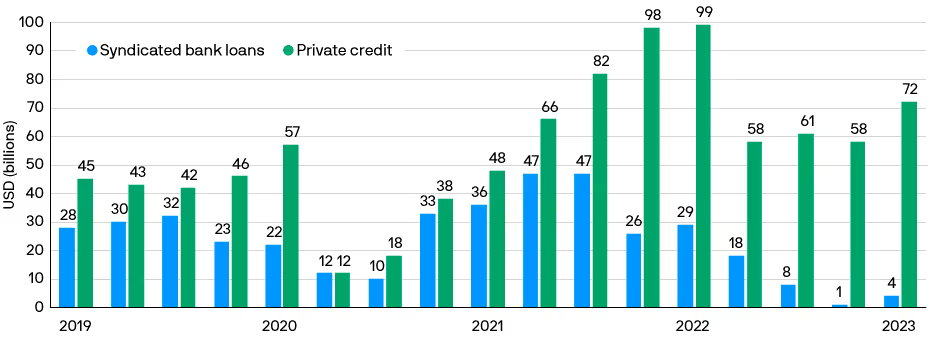

The Banking Exodus: A Sea Change in Lending

Banks are retreating from the lending space for various reasons, including increased capital requirements and reduced risk appetite. Exhibit 3 shows the quarterly issuance of bank loans and private debt, highlighting the shift:

Exhibit 3: Quarterly issuance of bank loans and private debt.

The Future: GPs vs. Banks - A New Paradigm in Lending

In the wake of ongoing banking crises that are eroding depositor confidence, General Partners (GPs) in the private credit sector are seizing the opportunity. Leveraging alternative, lower-cost capital sources such as insurance and evergreen funds, GPs are offering borrowers more flexible loan terms than traditional banks. This strategic shift is not just about filling a gap; it's about redefining the lending ecosystem. GPs are increasingly capturing a larger share of "investment-grade" quality loans, offering a win-win: better terms for borrowers and potentially higher, more stable returns for investors. In a nutshell, as traditional banks step back, GPs are stepping up, setting the stage for a new era in lending.

The GP’s promises of higher returns for lenders and better terms for borrowers are great. However, banks haven’t been the de-facto lender for the past 4000 years for no reason. The world of debt is complex and interlinked. We only have to look back 15 years to see the implications of this.

While age, size and regulation may sound like qualities of a fading incumbent, these features have contributed to the expertise of one of the world’s oldest industries. As new GP lenders emerge, investors should keep a tight eye on their underwriting experience and expertise.

The Crucial Role of Manager Expertise

"Manager skill in underwriting credit risk and executing transactions will likely become more valuable as higher rates increase borrower stress." - Jared Gross, Head of Institutional Portfolio Strategy, J.P. Morgan 2

In a world where Francisco Partners and TPG secured $2.65 billion in debt financing for their New Relic buyout from private lenders, the skill of underwriting credit risk is more crucial than ever. As interest rates rise, the stress on borrowers increases, making the role of experienced managers indispensable.

Conclusion:

The private credit market is a dynamic field with both lucrative opportunities and inherent risks. As interest rates rise, the sector is entering uncharted waters, with opportunities for those who know where to look. In this evolving landscape, the role of skilled managers and a diversified approach to investment can't be overstated.

Handpicking Stewards of Success:

In a world awash with investment options, our team sifts through over 220,000 global alternative funds to select top-tier investment opportunities. We aim for a balanced collaboration with our adviser and family office clientele, focusing on funds with a proven track record and a clear competitive edge. This ensures that we are partnering with trustworthy stewards of long-term capital commitments.

Get in touch with our team or sign up in minutes today to our platform and explore curated, top-tier global alternative investment funds that are right for you.

References

- Bloomberg (2023), Private Credit Loans Are Growing Bigger and Breaking Record. https://www.bloomberg.com/news/articles/2023-08-17/private-credit-loans-are-growing-bigger-and-breaking-records

- Jared Gross, JPM (2023), The paradox of private credit.

- Preqin (2023), Private Debt Q2 2023: Preqin Quarterly Update, https://www.preqin.com/insights/research/quarterly-updates/q2-2023-private-debt

* Past performance is no guarantee of future results. Past performance is not a reliable indicator of future results. Historical returns, expected returns, or probability projections may not reflect actual future performance.

Investments made available on the Stropro platform are only available to wholesale, sophisticated or professional investors and their financial advisers. Information contained in this email is general in nature. Please consider whether the information and investments are suitable for you and your personal circumstances. Stropro Operations Pty Ltd (ABN 28 633 603 399) (Stropro) is a Corporate Authorised Representative (CAR No. 1293257) of Stropro Compliance Pty Ltd (ABN 74 640 214 740, AFSL No. 533443). Stropro Operations Pty Ltd and Stropro Compliance Pty Ltd is a subsidiary of Stropro Technologies Pty Ltd (ABN 80 619 399 932) © 2021.

.png)