Stropro calculates percentage returns using a dollar-weighted (also referred to as a ‘money-weighted’) return methodology. A dollar-weighted return measures investment performance taking account of the size and timing of cash flows.

Investors, can control the timing of when they put money in or out of the portfolio. For this reason it is widely agreed that a dollar-weighted return is the most appropriate means of measuring performance from a private investor’s point of view.

Annualisation

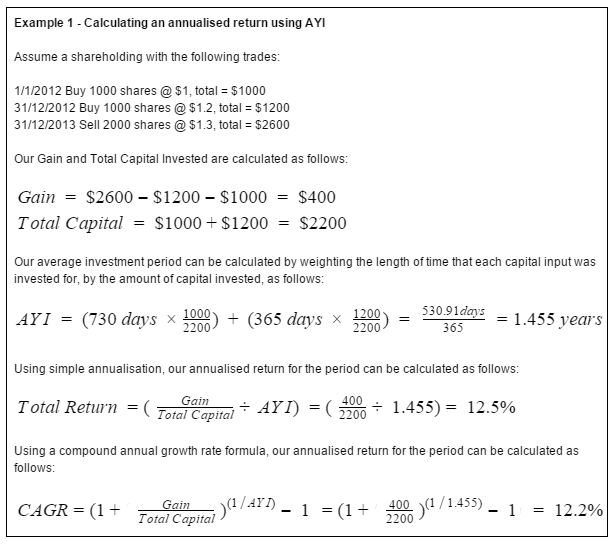

Stropro annualises returns weighting the length of time that each capital input has been invested for, by the amount of capital invested to determine the average years invested (AYI) for each dollar of capital. Example 1 below illustrates this calculation.

Returns can be annualised based on the principles of a simple annualised return or by using a compound annual growth rate (CAGR).

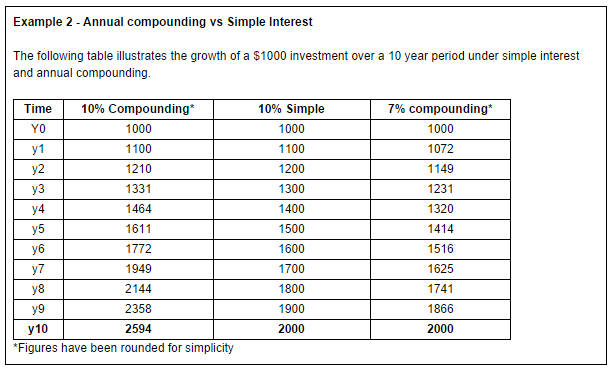

A simple annualised return simply divides the rate or return for the period by the number of years in the investment period. A compound annual growth rate calculates the year on year growth rate that would be required to achieve the same result. The table below provides an example of the differences between a simple annualised return and a compound annual growth rate.

The table in example 2 above illustrates that a 7% compound annual growth rate is approximately equivalent to a 10% simple interest rate over a 10 year period.

You can switch between these two methods in the settings for each portfolio. It’s important to understand which method you are using when comparing Stropro returns to other returns that you might see externally, such as an index or a fund manager. These returns are typically expressed on a compound basis when annualised over more than one year. We recommend you use the compound method when comparing your portfolio returns with other external returns.

Avoiding extrapolation of short term volatility

Due to the short term volatility that exists in the Sharemarket, returns can be misleading or difficult to interpret in some circumstances.

The most obvious circumstance is where a short term result is extrapolated due to the process of annualisation.

For example, a share that increased in price by 5% in the first day of ownership would result in an annualised return of 1825%. Equally, if the price decreased by 5%, the annualised return would be -1825%, which appears counter-intuitive since it’s not possible to lose more than 100% of your investment.

A more subtle form of extrapolation can occur even when the total investment period is greater than one year, especially where there is a large variation in the amount of capital invested during the period. For example consider a holding where a relatively small sum of money was invested for the majority of the investment period but with a large gain or loss on a much larger sum of money invested shortly before the end of the period. In this case the average years invested will be relatively small, which again results in an unintuitively large gain or loss percentage even though the total investment period may be greater than one year.

To avoid this problem Stropro simply divides the gain by the total amount of new, additional capital that the investor has contributed during the period. If this result is lower (in absolute terms) than the dollar weighted return, then a degree of extrapolation has occurred and the alternative methodology is used to offset this.

Notes

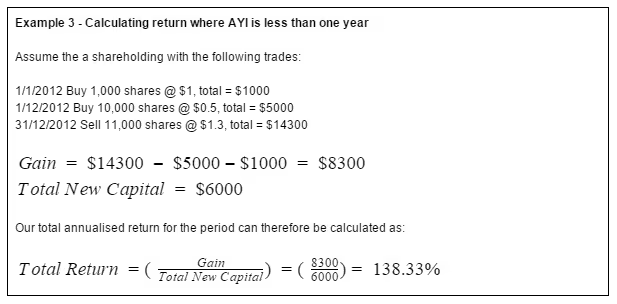

In the above example, the average years invested is only 0.23 years since the majority of the capital was invested for only one month. This results in a gain of approximately 600% using a dollar weighted methodology. This appears unreasonable since the large gain was clearly a result of short term volatility. A more reasonable perspective is to consider that the investor generated a gain of $8300 on $6000 total investment capital. The alternate methodology is only applied where it yields a more conservative figure (ie only when it prevents extrapolation a short term gain or loss). The test for this is: (total_capital * av_yrs_held) < (total_new_capital). By definition, this methodology is only applied where the AYI is less than one year (note that in the above formula, total_new_capital can equal but never exceed total_capital).

Component Returns

All percentage returns including component returns (dividend gain, capital gain and currency gain) are calculated using the same methodology as described above. When calculating component returns, the figures for the capital invested (denominator) and average years invested (AYI) remain the same, with the gain (numerator) varied accordingly.

It’s important to note that in the compounding context, the component return percentages will not directly sum to the total.

Important notes

1. There are various approaches to calculating a dollar-weighted return. Different methodologies rely on different assumptions and in some cases they may yield different results. The best-known method of calculating dollar-weighted returns is the Internal Rate of Return. This produces sound results in most cases but can produce unreasonable or even multiple results in some cases, and can sometimes fail to calculate a return at all particularly when there is extreme volatility and much variation in cashflows. Stropro instead uses a variation of the Modfied Dietz method which has proven to provide a reasonable measure of performance even with large volatility of prices and periodical cash flows. In most cases the return will be very similar to the IRR method. It is important to note however that no dollar weighted return methodology is free from limitations and therefore percentage returns should be used as a guideline and must be evaluated in the context of the chosen methodology.

2. Global Investment Performance Standards (GIPS) mandate that fund managers publish returns using time-weighted return methodology. A time weighted return differs from a dollar weighted return in that it explicitly ignores the impact of external cash flows. A time-weighted return is appropriate for measuring the performance of an investment manager on the assumption that the investment manager has limited control over when they receive funds from investors, or when the investor chooses to withdraw their funds. Stropro’s performance calculations are designed for use in evaluating the investor’s portfolio rather than a manager’s portfolio.