In Module 2 we dived into the mechanics of one of our popular investments – income-seeking structured products (or the ‘fixed coupon’ investment). This module will explore a popular variation that our clients utilise to enhance returns.

Introduction

Structured products are known for their flexibility. They can be designed to generate a return in any market scenario and they can be modified to suit a client’s objectives. Often, a client may not have an immediate need for an income stream, and instead prefer to receive a larger return at maturity – this is the case with the Accumulating Coupon investment. One of the reasons an investor may opt for this payment structure is to defer income for tax purposes.

Accumulating coupon structures maintain many of the features typical of an income-seeking structure, such as a knock-in level, a callability feature and tracking a basket of underlying assets. Module 2 provides definitions of each of these features if you need a refresher.

The main difference is how the return is paid to the investor. With an accumulating coupon, the coupon does exactly that, accumulates over a period of time and is paid out when a call event occurs or at the maturity of the investment.

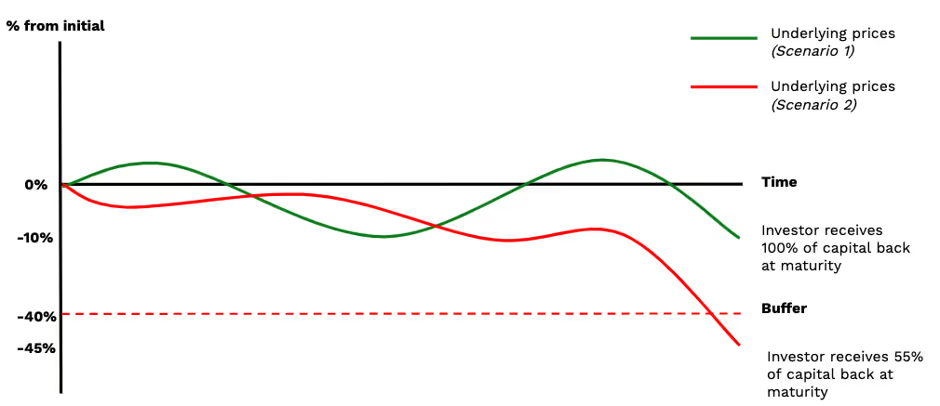

Let’s consider the below illustration:

In Scenario 1 the investment has matured and not breached the knock-in level (or buffer). The investor’s initial capital is returned and paid the accumulated coupon.

Example: Let’s consider a $100,000 investment that matures in 3 years with an accumulating coupon of 10% p.a. In Scenario 1 the investor receives $130,000. Or a total return on capital of 30%.

In Scenario 2, consider an investment where the knock-in level has been breached. In an accumulating coupon if the SP is knocked-in (buffer breached) the investor’s return is equivalent to the performance of the worst performing underlying asset.

Example: If the knock-in level was 40% and the worst stock is down 45% at maturity, the outcome for the investor is different to Scenario 1. An investment of AUD$100,000 would mean the investor would receive $55,000 of their capital back at maturity and no investment return. The investor therefore, has to make an assessment of the likelihood that any of shares will be down by 40% or more at maturity

Summary:

Important characteristics of a Structured Product with an accumulating coupon are:

1. The income is deferred in the accumulating coupon structure, which enhances the rate of return.

2. If a knock-in event occurs the investor forfeits any accumulated returns.

3. Returns from Structured Products with accumulating coupons tend to be taxed as capital gains not income. This can be beneficial to investors.

Investors need to consider the risks posed by the accumulating coupon structure and consider whether they are comfortable with the features of the product including credit risk of the issuer.

If an investor does not need regular income from the investment then a Structured Product with an accumulating coupon could be an option worth considering.

Ben Streater is Chief Product Officer for Stropro. This article is for educational purposes and is not a substitute for professional and tailored financial advice. This article expresses the views of the authors at a point in time, which may change in the future with no obligation on Stropro or the author to publicly update these views.

1. Based on the approach adopted by the ATO in TD 2008/21. Not taxation advice. Please seek the advice of a professional.