Key takeaways:

- The false truth of dividend yields could have Investors caught short if they continue holding onto expectations that company Boards will continue to pay out despite COVID-19s impact on their forward earnings.

- Many companies have begun the process of suspending dividends both globally and in Australia.

- The certainty of income can be secured by carrying the same exposure to the underlying assets, when invested as a structured product.

- A structured product provides the added benefit of buffering the investor against volatility.

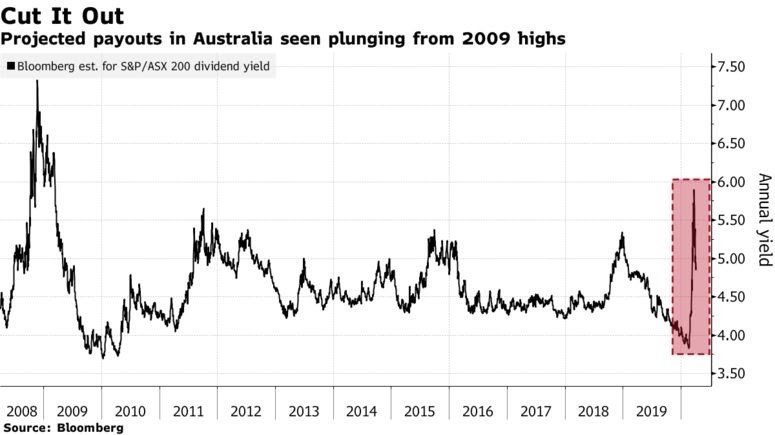

A major attraction of the Australian share market has been its high-dividend and tax effective paying stocks which Australian investors have grown accustomed to. With the onset of COVID-19 virus outbreak, this ‘investor mirage’ of high dividends, faces real risks due to two main factors unravelling in financial markets; 1) significant earnings pressure on companies and 2) significant push by regulators and central banks to suspend dividend payments for an undefined period to alleviate against foreseeable economic pressure.

On the 27th of March the European Central Bank (ECB) called on banks trading under its authority across Europe to stop paying dividends or the buyback of shares. Christine Lagarde, President of the ECB noted that this would allow banks to absorb losses and to continue supporting individuals, small businesses and corporates.

Similarly, On the 31st of March 2020, the Bank of England called on its major banks to suspend dividend payments to shareholders. Major banks including Lloyds, Royal Bank of Scotland, Barclays, HSBC and Standard Chartered, have now held back over $15BN in dividend payments. The Prudential Regulatory Authority in England, cited the following:

“….they are a sensible precautionary step given the unique role that banks need to play in supporting the wider economy through a period of economic disruption” (PRA)

On the 1st of April, the Reserve Bank of New Zealand has called on Australian Banks to suspend their dividend payments to support the large lending market they service in New Zealand.

Even though at this stage no announcement has been made in the Australian market to suspend dividends, the Australian Prudential Regulatory Authority (APRA) has put a note out to Australian Banks that any Board decision to pay out dividends in the next few months, would become at the behest of strong stress testing results and “this should nevertheless be at a materially reduced level’’.

If the pandemic continues to weigh on the economy, and Australia does follow suit like other economies. Fiona Balzer, from Shareholders Association of Australia, noted that ‘’… hundreds of thousands of self-directed investors could be forced onto the welfare state, to make up for the lost income in the form of franked dividends’’.

Christopher Joye, from Coolabah Capital Investments notes “I expect one of the majors to potentially defer its half-yearly dividend to focus on prudently building capital while the two others that report soon will probably pay a substantially reduced distribution. All of this is “credit positive” for depositors, bond-holders, and hybrid investors”.

However if Australian banks are well capitalised and no drastic steps are taken to suspend dividends, it is clear that rather earnings pressure could act as ultimate lever for dividend reductions. Macquarie Group has reduced 2019-20 dividend forecasts for 73 of 182 Australian stocks, noting potential shifts of final year dividends as well.

The first indication that this revision is coming would be in the form of a notification to the ASX that they intend to suspend future guidance around earnings. This is a real indication that forward earnings have just become too unpredictable and uncertain to forecast with any reliability. Without this reassurance of what they expect to earn, any payment of dividends comes under very real risk of being suspended.

For many Australian investors, dividend reductions are not new. In 2019 Australian banks started cutting dividends due to a combination of factors; added margin pressure from consistently low interest rates, remediation costs from the Royal Banking Commission and increased capitalisation requirements. One can only anticipate that with COVID-19, increasing loan impairments and continued downward pressure on interest rates due to quantitative easing, will only add continued pressure on dividends. This is not withstanding the downward pressure on investor capital as companies begin to report lower earnings.

Given the above, the investor impact will be two-fold. The first is pressure on the dividends and therefore reduced income and consequently the difficulty for the underlying stock to maintain its value. Secondly, the total-return i.e. the income (dividends) received along with the share price (capital gain) correction could be significant that there could be a severe drag on investor portfolios. However for the investors that have been investing into structured products on the Stropro platform, there is a solution to these highly probable outcomes.

The fixed coupon series provides the investor enhanced and fixed returns, with downside protection to buffer against volatile markets. One of these investment opportunities closed recently. This investment has exposure to the four (4) largest banks in the United States by Tier 1 Capital; Citigroup, JP Morgan, Bank of America and Wells Fargo & Co. Investors were able to lock-in an 8% p.a. fixed coupon, paid as quarterly distributions. Additionally, they were given a 40% buffer to protect against further downside in the US Banking sector (observed at maturity). In this type of investment, our investors are not guessing what their income return will be.

From a risk-adjusted return basis, investors should consider structured products in their portfolio, to minimise downside risk. More importantly, the solutions provide a way to achieve greater certainty in the form of a coupon payment, thereby protecting their portfolio yield, which they have become accustomed to. With the economic and company earnings outlook even more uncertain as the world battles through the COVID-19 crises, those investors who hold exposure to income generating structured products will take comfort and have peace of mind that their ‘yield strategy’ is secure for many years to come.

Stropro is an investment platform for wholesale and sophisticated investors where you can access Structured Products issued by investment banks. The tactical investment opportunities we arrange are generally defensive and focused on generating enhanced returns regardless of the economic conditions. In times of economic volatility these Structured Products can be particularly attractive. Our view is that Structured Products belong in all sophisticated investor portfolios and should make up approximately 5% of your portfolio allocation.

Anto Joseph is the Chief Executive Officer of Stropro. This article is for educational purposes and is not a substitute for professional and tailored financial advice. This article expresses the views of the authors at a point in time, which may change in the future with no obligation on Stropro or the author to publicly update these views.