As an investor, you are likely concerned by recent market volatility and are considering how to navigate this uncertainty. Doing nothing and resisting your “inner Buffet” may be wise, however we discuss a tactical strategy to “sell volatility” that can deliver enhanced returns whilst providing an enhanced income stream.

Investment market volatility presents opportunity?

Heightened volatility presents opportunities for sophisticated investors that are positioned to take advantage in uncertain times. As explained further below, experienced investors may be familiar with the concept of “selling volatility”; during times of market disruption, such as the current pandemic and oil price war, volatility spikes and investors can generate enhanced returns with tactical investments.

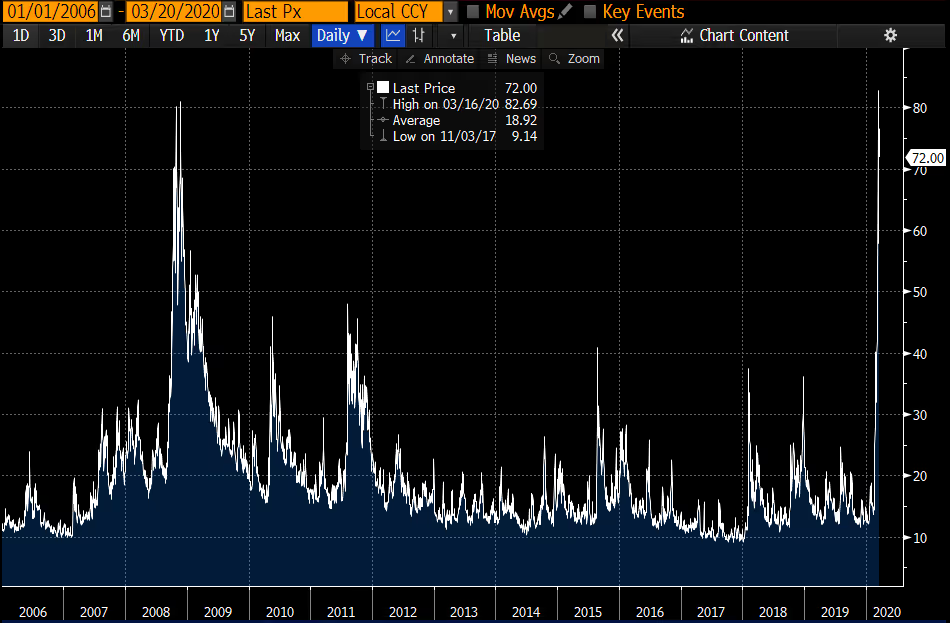

Volatility is a key indicator of uncertainty. Technically, volatility is a statistical measure of the dispersion of returns for a given security or market index. In simple terms volatility measures how much prices are moving around. In stable markets volatility is low, but currently with the future outlook uncertain, volatility has spiked. A well recognised measure of volatility is the VIX index which has recently reached GFC-level highs.

Sell volatility strategy

From a traditional “buy and hold” perspective, experienced investors know that ‘picking the bottom’ is a difficult task. So rather than speculating on timing an entry to buy, investors can implement a “sell volatility” strategy through instruments such as income generating Structured Products.

The global Chief Investment Officer for Citigroup Private Bank, David Balin, recently highlighted the popularity of this strategy in an interview with bloomberg;

“Another popular note [Structured Product] sells volatility to create income. The client needs to assume market risk if the underlying index falls to a level, say 25% below today’s price. We did more than $100 million in such structures last week.”

What is the sell volatility strategy

To elaborate on this straegy, the investor is purchasing a Structured Product issued by an investment bank. The product tracks the performance of an underlying basket of shares or indices and in return the investor receives a regular income stream. An investor may further enhance the return, if they forgo the regular fixed income stream and opt for the return to be accumulated and paid at maturity, this approach also provides favorable capital gains tax treatment.

These Products are particularly attractive during times of market volatility because the premium paid on the options embedded in the product increases, which in turn increases the coupon paid to the investor.

To provide an example, in early February 2020 we priced a defensive income opportunity linked to the top 4 US Banks that returned 4% p.a. paid quarterly. Currently the same opportunity is paying 8% p.a. double what it paid one month earlier. Investors who “sell volatility” during volatile economic periods benefit two-fold:

1. Protection is heightened due to significantly lower asset values; and

2. Income returns are enhanced by selling volatility at record highs.

Stropro is an investment platform for wholesale and sophisticated investors where you can access Structured Products issued by investment banks. The tactical investment opportunities we arrange are generally defensive and focused on generating enhanced returns regardless of the economic conditions. In times of economic volatility these Structured Products can be particularly attractive. Our view is that Structured Products belong in all sophisticated investor portfolios and should make up approximately 5% of your portfolio allocation.

For further information contact team@stropro.com

* It is important to note that the investor’s capital may be at risk should a predefined buffer be breached as per the terms of the offer, and capital is subject to credit risk of the issuer.

Ben Streater is the Chief Product Officer at Stropro. This article is for educational purposes and is not a substitute for professional and tailored financial advice. This article expresses the views of the authors at a point in time, which may change in the future with no obligation on Stropro or the author to publicly update these views.