The economic shock brought on by the COVID-19 crisis has directly impacted corporate earnings, resulting in dividend slashing and job losses, writes Stropro Chief Product Officer Ben Streater.

This is translating into bearish economic sentiment and is driving expectations that markets will continue to experience increased volatility in the short-term.

On a positive note, in the long-term markets are expected to recover strongly based on fiscal and monetary stimulus from governments and medical research to produce the COVID-19 vaccine.

It might be time to consider an investment strategy that factors in another downturn before a strong recovery phase.

The ‘W’ recovery

In recent weeks, several economists and business leaders like former Westpac boss David Morgan have suggested the economy may not bounce back as quickly as some investors expect.

Changing consumer preferences, poor business and consumer sentiment, rising debt levels and the unique nature of this crisis all point to a W-shaped recovery.

This implies a ‘double dip’ sloped recovery, rather than a ‘V’ or ‘U’ shaped recovery. The central case behind forecasting a ‘W’ is due to a cold turkey end to aggressive stimulus packages such as JobKeeper and JobSeeker.

Extending these and other support programs would likely soften the economic shock but will come at the cost of rising deficits and debt levels.

There is now growing momentum behind this theory, backed by the belief that a quick recovery is very unlikely, given the huge amount of disruption and debt it has taken to flatten the curve of the COVID-19 contagion.

While investors may be riding the recent equity rebound, history shows us that strong market rallies following a sharp decline are a recurring pattern.

Even a dead cat bounces

All investors should be weary of the dead cat bounce, a temporary recovery of asset prices from a prolonged decline or a bear market that is followed by the continuation of the downtrend.

The problem is these can be difficult to spot. Particularly when investors start believing that the market has returned, and that things will soon return to normal. It is becoming increasingly evident that ‘normal’ will look very different in the future.

The recent economic slowdown was an engineered response to a health pandemic, not a recession triggered by financial markets. It is easy, therefore, to believe that once the virus is contained and a vaccine found that the economy and financial markets will return to ‘normal’.

Investors with money in the market will have a positive bias towards this logic but what we are seeing in markets may turn out to be the dead cat bounce. Former Westpac CEO David Morgan, AO, recently highlighted the unique nature of the current crisis and its lasting impact on different industries and consumer and business sentiment.

A strategy for our times

Considering these observations, Stropro has devised an innovative strategy for investors that we’re calling the ASX 200 Growth Optimiser – a structured product issued by a global investment bank and linked to the performance of the S&P ASX 200 index.

The investment aligns to a long-term optimistic view of market recovery while capitalising on potential volatility in the short term.

It optimises the total return for the investor by capturing the lowest price of the ASX 200 for the investor, removing the need to ‘time the market’. This is particularly relevant for those investors who are looking for passive exposure to the ASX 200 index.

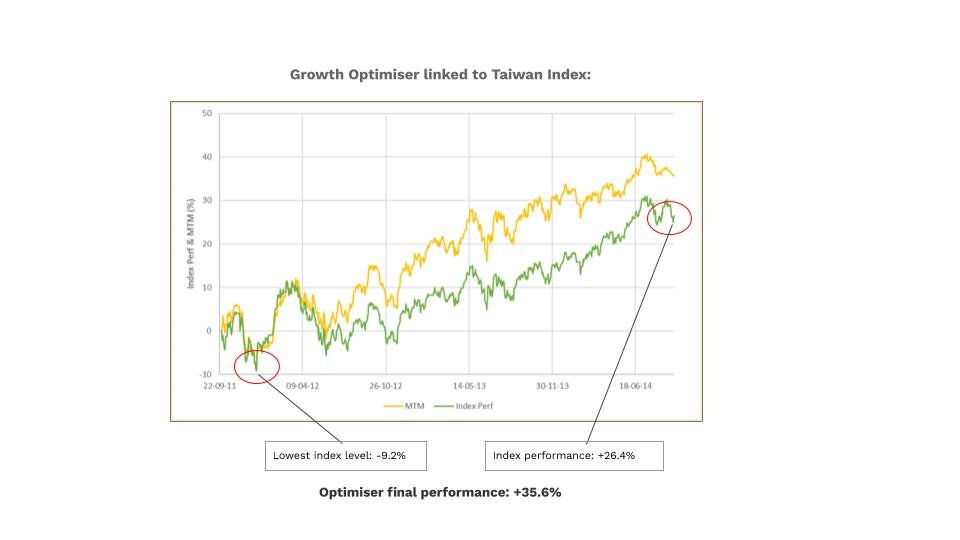

I was recently made aware of high net worth investors who were able to capitalise via a similar strategy linked to the Taiwan Index in 2011.

Summarised below are the observations and outcomes:

· The green line is the performance of the Taiwan index (TWSE) over a 3 year period.

· The yellow line is the daily valuation of the structured product linked to the index.

· The lowest level of the index was observed on 19th December 2011 which was -9.2% from the initial level

· At maturity (3 years), the index finished +26.4% above the initial level.

· Investors in the structured product received a return of +35.6%

The Structured Product outperformed the return of the index by capturing the lowest point of the index over the 3-year term.

If investors believe in the “W recovery” and that the ASX200 will experience short term volatility but are optimistic about a longer-term recovery over 3 years, then this Structured Product will outperform a passive investment strategy.

If this view does not materialise, investors would still receive the direct exposed to the performance of the index over three years.

About Stropro:

Stropro is Australia’s dedicated investment platform for Structured Products. The Stropro platform is available to wholesale and sophisticated clients, financial advisers and family offices. For decades across the globe, high net worth investors have been utilising structured products to enhance income, buffer volatility and increase portfolio diversification. In Australia, these exclusive investment solutions have typically been restricted to private bank and institutional investors, until now. Stropro partners with global investment banks to democratise their capability. Because of these partnerships, our clients benefit from global research and access to exclusive tactical investment opportunities. We look forward to bringing you the benefits of Structured Products from the world’s leading Investment Banks.

.avif)