Still hunting for yield? Our thoughts on the risks and opportunities in 2021.

![]() Anto Joseph on 14 May 2021

Anto Joseph on 14 May 2021

Income generation is an important driver for many investor portfolios and is often the top priority when it comes to assembling a long-term investing strategy.

With Australia’s official cash rate at a record low, and according to economic forecasts likely to stay close to zero for the next three years, investors are struggling to find yields higher than what is being delivered in savings accounts or term deposits. The push to secure higher yields has meant that investors are taking a riskier approach to investing than they usually would, shifting from cash and term deposits to equities, high risk bonds, or unlisted investment trusts, to meet their income needs.

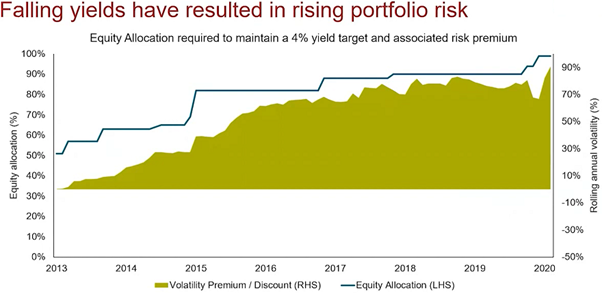

Falling yields result in rising portfolio risk

In the below graph Vanguard demonstrates what portfolio allocation percentage would need to be in growth assets (for example, equities) compared to defensive assets (for example, cash) to earn a 4% income return. In this example, the required portfolio allocation into growth assets increased from 50% in 2015 to almost 100% in 2020 to achieve a 4% yield. Consequently, an investor would have doubled their risk exposure to earn the same amount in income. The problem with moving up the risk curve into growth assets (like equities) is that the probability of a capital impairment increases considerably. In fact, if you look at the S&P ASX 200 over the next 8 years, the probability of loss is approximately 15.1%1.

Source: Vanguard

Yield hunting has become an Australian sport

Difficult market environments distort the perception of risk and can lead investors to shift their investment exposure; i.e. deploy capital into riskier assets with the objective to generate higher income. Let’s examine the conversations taking place...the current state of dividend and property yields as an example.

Aussie dividends under pressure

Dividend yields have fallen sharply and are expected to remain low in the near term. Traditionally, the big four banks have paid the largest dividends but that source of income has been slashed as the banks hang on to as much capital as they can to weather the COVID-19 storm. And it is not just banks that have been slashing dividends – other typically ‘safe’ companies including building products maker James Hardie (ASX: JHX), financial services company Challenger (ASX: CGF), Qantas (ASX: QAN), Transurban Group (ASX: TCL) and Sydney Airport (ASX: SYD) have either ditched dividends entirely or slashed them.

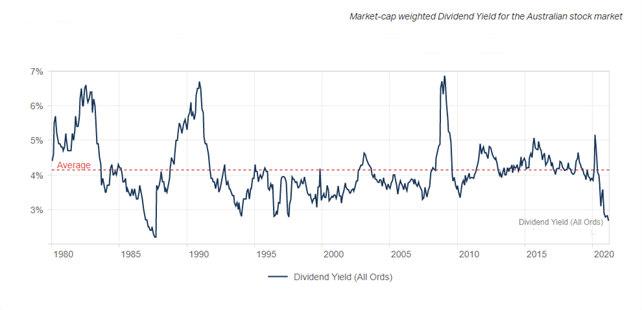

The chart below shows the trailing grossed-up dividend yield of the index for the past 20 years.

The dividend yield on the Australian equity market (as shown above), has fallen considerably below the historical 4% average, now sitting at a mere 2.80% p.a. This has resulted in investors adding higher-yielding stocks to their portfolios outside of the traditionally blue-chip options. By employing this strategy, it leaves investors open to portfolio concentration in high yield, low quality assets, which can be detrimental in volatile markets. Dividend yields can often be distorted by a sudden drop in the share price, which makes the ‘implied’ yield look attractive, yet over time a more realistic reflection of the real earnings becomes apparent and these dividend payments don’t materialise.

So are Aussie property yields

The property market has delivered lucrative capital growth returns for many investors and with the cost of credit at historical lows and home buyer incentives, future growth seems sustainable. The significant constraint to the pace of that growth is population growth as immigration has slowed considerably. Additionally the current yield on residential property in Sydney and Melbourne has fallen considerably to levels of around 2.90% p.a, making it potentially less attractive to increase exposure.

For investors who use A-REIT’s to obtain property exposure the concern has been around volatility putting a cloud over REIT distributions. This has been driven by fears of rising vacancy rates in commercial and retail property and the need to provide higher financial incentives, such as rent free periods, to attract tenants. As many REITs are currently trading at share prices well below their NAV, yields are currently quite high for many REITs. So, it’s important to be aware that a particularly high yield for a REIT may sometimes reflect a disproportionately high risk.

Furthermore, REIT yields are not guaranteed, as the Global Financial Crisis (GFC) demonstrated - between 2007 and 2009 the Australian REIT index fell by 77% and it is still recovering.

Hunting income with clarity

Despite the current low yield environment, opportunities for enhancing returns across broader asset classes do exist. Constructing the optimal portfolio whilst weighing risk and return is quite challenging for the majority of investors to achieve. At Stropro, we help our clients invest smarter by providing them with various investment opportunities to navigate volatility and achieve better clarity of their return. Since launching the Stropro platform in late 2019, our clients have navigated the COVID-19 turmoil using products which enhance income, provide a level of downside protection from volatile markets and be complementary to traditional investments.

Some of the benefits of these products include:

A defined rate of return and more clarity on risk.

Carrying the same exposure to the equities, but with the added benefit of buffering the investor against volatility.

Diversification into global assets that may be otherwise difficult to access

How Stropro is helping clients enhance returns

Investors as well prominent commentators have expressed concerns about inflated equity markets, challenges of accessing lower-risk income solutions, and growing geopolitical uncertainty.

“Ongoing fiscal stimulus, strong growth and low rates all remain supportive of Australian shares, notwithstanding the high risk of a short-term correction” - Dr. Shane Oliver, Chief Economist, AMP Capital.

In response to this, Stropro has arranged the ‘ASX 200 Linked Investment’ from a top tier global bank. The product provides a defined return, downside protection throughout the term to navigate volatility and based on 20 years of back testing, the investment has a 0.00% historical probability of loss2.

This investment opportunity is available via Stropro’s investment platform and is open to sophisticated and wholesale investors. If you would like to become a client of Stropro and access further details of the ASX 200 Linked Investment along with other investment strategies click here.

Sources:

1. Bloomberg Terminal, historical data from 1st Jan 2000 to 4th May 2021. Assuming normal distribution for the ASX 200.

2. Bloomberg Data, 5th May 2021. The strategy was back tested over a 20 year period. Past performance is not a reliable indicator of future performance.

Links:

https://www.afr.com/wealth/personal-finance/asx-s-yield-attraction-to-remain-strong-20200629-p5577e

https://smallcaps.com.au/stocks/?symbol=CGF

https://smallcaps.com.au/stocks/?symbol=QAN

https://smallcaps.com.au/stocks/?symbol=TCL

https://smallcaps.com.au/stocks/?symbol=SYD

https://sqmresearch.com.au/property-rental-yield.php?region=vic%3A%3AMelbourne&type=c&t=1

https://www.afr.com/wealth/personal-finance/a-reits-primed-for-growth-in-2021-20201210-p56mfy

https://www.afr.com/wealth/personal-finance/asx-s-yield-attraction-to-remain-strong-20200629-p5577e

This article has been prepared by Anto Joseph. Anto Joseph is a director of Stropro Operations Pty Ltd (ABN 28 633 603 399) (Stropro). This article is for educational purposes and is not a substitute for professional and tailored financial advice. This article expresses the views of the author(s) at a point in time, which may change in the future with no obligation on Stropro or the author to publicly update these views. This article uses information from sources the author considers to be reliable but does not represent that such information is accurate or complete, or that it should be relied upon. Past performance is not a reliable indicator of future performance. Investments may rise and fall in value and returns cannot be guaranteed. Stropro makes no representations or warranties, express or implied, are made as to the accuracy or completeness of the information it provides. Stropro is a Corporate Authorised Representative (CAR No. 1277236) of Lanterne Fund Services Pty Ltd (AFSL No. 238198).

Subscribe to our newsletter

Get the latest articles and updates on Stropro’s products delivered straight to your inbox.